As two of the top U.S. cable providers, Comcast (NASDAQ:CMCSA) and Charter Communications (NASDAQ:CHTR) each sit at the intersection of several big-ticket trends shaping the media, cable distribution, and telecom industries.

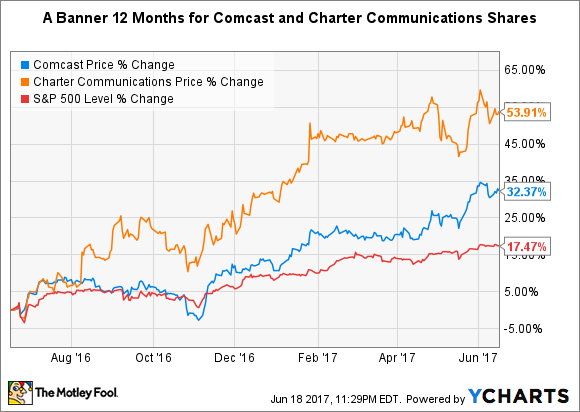

Their shares have each eviscerated the S&P 500's impressive performance over the past 12 months.

However, though the recent winner between these two rivals is clear, let's take a bigger-picture view of Comcast and Charter Communications through a three-part analysis.

Financial fortitude

The cable distribution industry operates under a unique set of rules, as these four important measures of solvency and liquidity for Comcast and Charter suggest:

Company | Cash and Investments | Debt | Cash From Operations | Current Ratio |

|---|---|---|---|---|

| Comcast | $4.0 billion | $61.7 billion | $19.5 billion | 0.8 |

| Charter Communications | $2.9 billion | $62.8 billion | $10.4 billion | 1.3 |

DATA SOURCE: YAHOO! FINANCE

Comcast and Charter share more similarities than differences when it comes to their financial structures. More to the point, there isn't a meaningful difference between the two in terms of their cash and investments, debt, or current ratio.

However, Comcast's cash flow-producing capacity is a key advantage over Charter. Granted, generating $10.4 billion in cash from operations is nothing to sneeze at, but the basic arithmetic lies in Comcast's favor here. As the leader in the only point of differentiation between the two in this segment, Comcast deserves a win, though both companies appear to be in fine financial condition.

Winner: Comcast.

IMAGE SOURCE: GETTY IMAGES.

Durable competitive advantages

Comcast and Charter generate the bulk of their revenue by providing the same three core services -- cable video, internet, and phone -- to consumers and businesses across the United States.

What's more, Comcast's and Charter's customer bases are virtually the same size. Comcast's 10-K filing shows 28.6 million total customer relationships at the end of its fiscal 2016, compared with 26.2 million for Charter.

However, the defining difference between the two lies in Comcast's ownership of significant media assets -- including NBC Universal TV's motion-picture content production, a cadre of local TV stations, and a theme-park operation. All told, these businesses contributed 39% of Comcast's consolidated revenue in 2016. Charter's business model controls just the "pipes" that deliver various telecom services to consumers, whereas Comcast controls the pipes and some of the content that flows through them.

Comcast and AT&T are both said to be preparing to introduce over-the-top cable services that flow directly to consumers' mobile devices, to counter similar services from a host of tech companies. That development would only strengthen Comcast's strategic position over Charter. Comcast is in a better position to launch its own services thanks to the leverage its content assets provide it. So while Charter is no slouch, Comcast earns a win here.