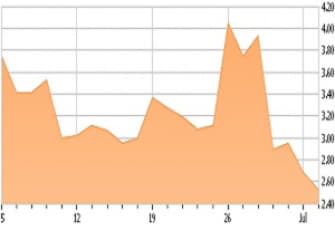

Rite Aid (RAD) has become a trap for hopeful bulls that are either buying shares at what they perceive to be low prices or are holding onto or adding to positions held in anticipation of Walgreens (WBA) merger approval. Owning RAD right now appears to have an opportunity cost that outweighs its upside potential, at least in the short-term and I see little reason to be holding shares at the moment.

It appears investors are thinking that after dropping following the announcement of a store deal with Walgreens rather than a merger, RAD shares are now cheap. This is far from the case. As I wrote in my most recent article on the stock, there doesn't appear to be sufficient operating performance to warrant even the current depressed price level.

According to analyst estimates from Yahoo! Finance, RAD trades at 30 times fiscal year 2018 earnings. With a market capitalization of around $3 billion, an initial look might have indicated that RAD seems cheap considering the $5.4 billion cash infusion it just received, but the $7 billion debt position implies otherwise. This begs the question: why are RAD shares trading at levels above its peers?

READ FULL ARTICLE HERE